On Investing: Keep It Simple

Looking past the noise and distractions

Whether it’s your professional trade or something you do on the side, the chances are that the longer you’ve spent navigating financial markets, whether in a small or big way, you'll likely have been humbled by them in some way or another.

I know I have, and many times at that.

And while I continue to try and learn from my mistakes, I’m always on the lookout for ways to diversify my approach without overcomplicating things. It often feels like an effort spent in vain.

Investing is anything but simple.

Yet, there never seems to be a shortage of content online and on social media, including from many popular influencers and content creators who produce highly entertaining pieces that sometimes allude to a world of investing made easy.

Due to people's shorter attention spans (not a good thing!) and the way many of these platforms incentivize and reward creators, much of this content often lacks the necessary details and context and, as a result, can be risky to act on in a vacuum.

What many think is "investing" may only come to find out that they’ve actually been engaged in plain old speculation. There is a big difference.

Investing is anything but easy.

And when things inevitably go south, we’re unapologetically reminded that we should have known better and to always "do our own research."

It’s obvious that we need to take responsibility for our own actions and be thorough in informing ourselves before making a decision, but at the end of the day, this shouldn’t be an excuse to push out poor content.

The Internet as a financial guide and resource

While many will say that you shouldn’t take financial advice from anyone online, I still believe that the Internet is an invaluable resource that can improve your knowledge and capabilities.

It’s almost silly not to take advantage of it when you think about it. However, you do need to have a healthy dose of skepticism with anything you read, listen to, or watch online.

Particularly for newer investors, or for anyone who doesn’t do this for a living (like me!), a concerted effort to move past all the noise and distractions of “easy investing” is often in our best interest.

The last place you want to end up is being caught up in a hype cycle, only to find yourself in "fear of missing out" on the next big "sure thing" without really knowing what you’re doing apart from apparently "getting rich quick."

In hindsight, it’s obvious why this doesn’t work for most people.

Having a better understanding of the fundamentals can really help with seeing past these distractions, and improving your familiarity with investment philosophies and frameworks can be a good starting point.

Economies and markets tend to be cyclical, with the news and hype of the day reflecting the sentiment of what traders and investors are facing in a particular business cycle stage. It is often all over the place and sometimes even nonsensical.

Having an investment framework can help guide your decision-making, as you’ll have a view in terms of your financial goals and expectations, risk appetite, and time horizon.

These can range from top-down (i.e., invest based on macroeconomic trends) and bottom-up (i.e., focused on company-specific fundamentals), to value (i.e., looking for undervalued stocks) and growth (i.e., looking for above average growth) investing, and being an active (i.e., shorter-term) or passive (i.e., longer-term) investor.

Improving your knowledge of these concepts and figuring out which may better align with your own understanding and beliefs, as well as your financial situation, can really help cut through a lot of the noise.

It can also help you find credible and respected sources online who tend to be thought leaders in their respective areas. Most of the time, they will have a track record of making helpful and informative content, and they will be verifiable professionals or experts in their fields.

There are many of them out there, so it does take time and effort to get to know them, including how they interact with their communities and how they react when they’ve made a mistake. All of these smaller details matter before you decide to learn from their content and potentially take on some of their advice.

The broader your understanding, the wider your perspective. It goes without saying that you don’t need to pick one philosophy over another. As much as we would like, there isn’t a single approach that necessarily outperforms the rest.

The sooner you invest, the better (usually)

A word of caution

If there is one principle that almost everyone subscribes to, it’s that the sooner you get started, the better.

As they say, "It’s not about timing the market, but time in the market."

And while there’s truth in this, it can instill a sense of urgency in anyone who feels like they may be late to the game, resulting in them jumping into the deep end, which can end badly.

There are obviously caveats to this principle.

A critical one being that it can't be any kind of investment but rather investments in high-quality assets. That is, assets that are regulated and have been around for some time, signaling reliability and confidence in the eyes of investors. Many of the popular US stock market indices and bond markets are often cited as examples.

In addition, it’s important from a personal standpoint that:

You’re financially stable in terms of having sufficient savings set aside and a secure source of income; and

You understand the risks involved in whatever you’re investing in.

No matter what historical data or market analyses say, past performance is not necessarily an indicator of future returns.

Investing is largely about managing risk and increasing the chances for the best possible returns given the circumstances.

A way to get started sooner

As previously mentioned, US stock markets generally comprise higher-quality investment opportunities when looking at publicly traded companies. The S&P 500 is one of the most popular indices out there. It tracks 500 large companies listed on US exchanges that meet its criteria.

It tends to be the one that most investors and funds benchmark themselves against to determine whether they’ve “beaten the market” for any given period.

Performance data on the S&P 500 goes back to its inception in 1928. It should also be noted that while the index started in 1928, its tracking of 500 companies as part of its current approach only began in 1957.

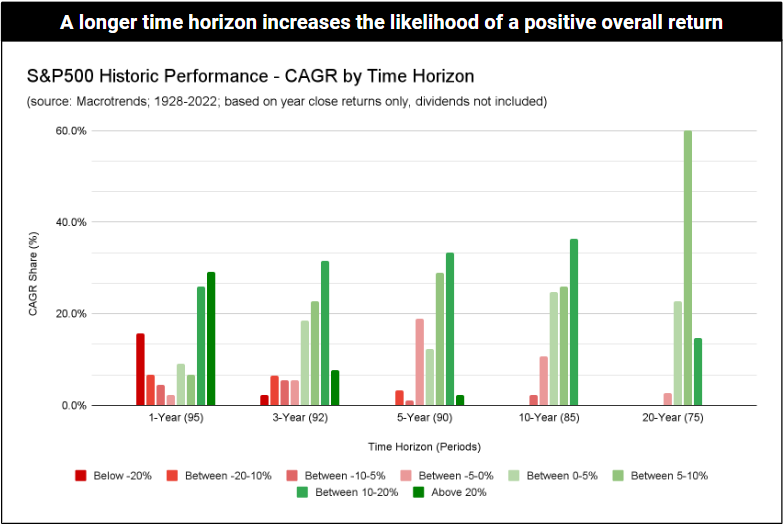

So what does the data say?

When we look at 95 years’ worth of data in terms of compounded annual returns (dividends not included) across different time horizons (e.g., 3 years, 5 years, 10 years, etc.), the first graph below shows a clear trend towards more periods of positive but lower returns over time (less red, more light green).

As an example, if you looked at any five-year period during the S&P 500’s existence, there was a near one-in-five (19%) chance that you may have seen a negative return of up to 5% over that time horizon. That is, negative returns of between 0% and 5% happened in 17 of 90 five-year periods.

Meanwhile, looking at a 20-year time horizon, you would have had a 60% chance of seeing a positive return between 5% and 10%. There were only two 20-year periods where you would have experienced low negative returns, all the way back in 1948 and 1949.

In fact, if you had invested in the S&P 500 at any point between 1928 and 2002 and held it for 20 years, you would have had a 97% chance for a positive return.

That’s pretty close to 100%. Was there any time horizon with only positive returns? Yes, at 24 years and beyond, the S&P 500 would have provided only positive returns.

And it's not just the increased likelihood of a positive return as the time horizon lengthens; it's also how rates of return change. If you look at the second graph below, the best and worst returns drastically decrease over time.

While annual returns of 46% and 28% sound like a dream, decreases of 47% and 31% are what nightmares are made of. You’ll notice that the occurrence of more extreme negative returns decreases faster than more extreme positive returns. This is in addition to average return rates remaining within range of each other (between 6.7% and 7.7%) no matter the time horizon.

Historic data on indices, like the S&P 500, really do build a compelling case for investing sooner. Sooner in the sense that you’re more likely to be able to hold it for longer, therefore increasing your chances for an overall positive return.

But average rates between 6% and 8% don’t seem particularly attractive, especially in light of inflation rates in the US averaging around 3% per year over the same period.

Well, the numbers above only show returns from the price appreciation of the S&P 500. If we include dividends, then the average annual return (not compounded) is closer to 11.5% between 1928 and 2022.

Through the power of compound growth and having faith that past performance has some level of indication for future returns, if you found a way to invest $10,000 every year in an index fund tracking the S&P 500 over 30 years, you’d see an investment of $300,000 return nearly $2.2 million (not accounting for fees and taxes).

Final thoughts

Does this mean you should only invest $10,000 a year in an index fund tracking the S&P 500? No, of course not. It really depends on your own personal circumstances and goals.

There are always going to be risks involved. The analysis above can provide some comfort in knowing that the longer you’re invested in a high-quality asset, the higher the chances for a solid positive return.

Investing long-term in equities, like the stock market, usually comprises one component of a diversified investment portfolio. It’d be wise to have a view on other asset types, like bonds and commodities, to help balance things out and weather any unexpected storms.

But it takes time to figure out what kind of investor you want to be and which investing philosophies resonate with you. And that’s perfectly fine.

While you’re figuring things out, there are “simpler” approaches out there that you can begin working on in the meantime that are more likely to benefit you down the line, no matter which direction you head in.

Just don’t get distracted by the noise.

See you in the next one!

If you’re interested in reading my thoughts on the basics of finance and investing, take a look at a three-part series I wrote awhile back below:

And great S&P historic performance chart, let's see if we can find one with dividends included to make it even better. Thank you!

Great take! Figuring out what fits to one is the most time consuming and hard part ... once that is set, things are way more easy and efficient and in some cases automatic. Cheers!